| Contact |  |

|

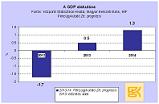

Forecast - Hungarian Economy (2011-12)

If one quarter of the foreign currency loans (HUF 5200bn) are affected by the government?s plan, banks would suffer a 20-25% loss (HUF 250 bn). The Hungarian banks had only HUF 10-12bn profits last year (mostly the Hungarian OTP).

The move will further deteriorate their lending position.

(Between 2010-2011the decrease of corporate lending was HUF 700 bn, private lending decreased by HUF 450 bn.)

We expect a modest 1% GDP-growth for 2012 (due to net export only) but could not exclude recession.

The Government?s measures did not support recovery.

The flat personal income tax hit a HUF 500bn hole on the budget but did not stimulate domestic growth. While the government attempted to stimulate demand the effects of foreign currency loans and the characteristics of the labour market were largely ignored .

The public works program (however wrong) is 1-1.5 years late.

PPP investments were halted for inspection.

Retroactive crisis taxation eroded the rule of law, worsened the banks? lending position and destabilized the business environment.

The lack of concept shines through all the measures of the government. Hungarian risk premium has been higher than during the previous government.

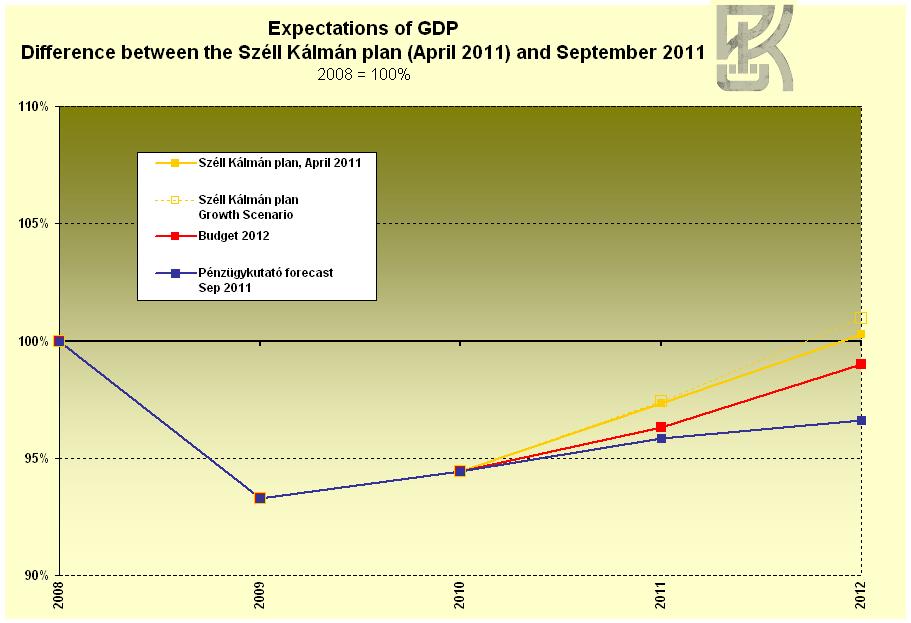

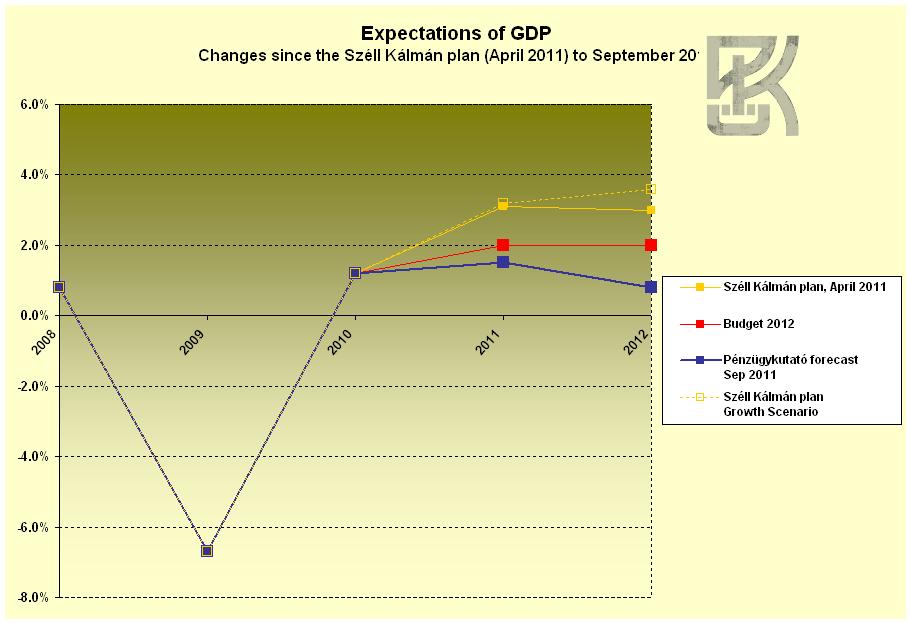

The 2011 budget revenues are overestimated by HUF 130-140bn while the Széll Kálmán Plan was not executed. The HUF 550bn austerity measures in the Plan seem unlikely to happen.

The further announced HUF 200bn austerity will not be enough due to the optimistic revenue estimation.

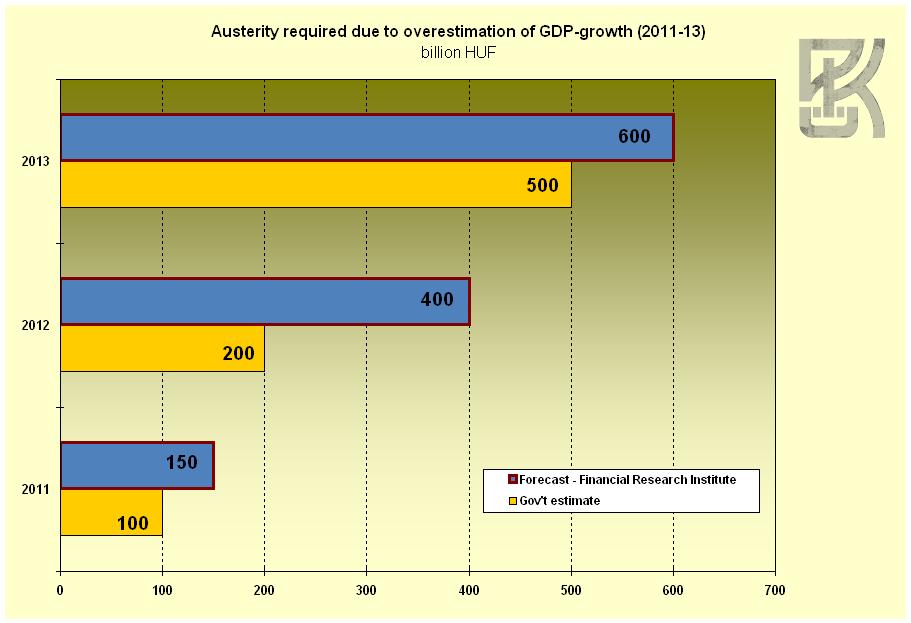

We expect the need for a further HUF 204bn austerity for 2012 in order to keep the 2.5% deficit target.

Fight against inflation merely meant the freeze on utilities bills.

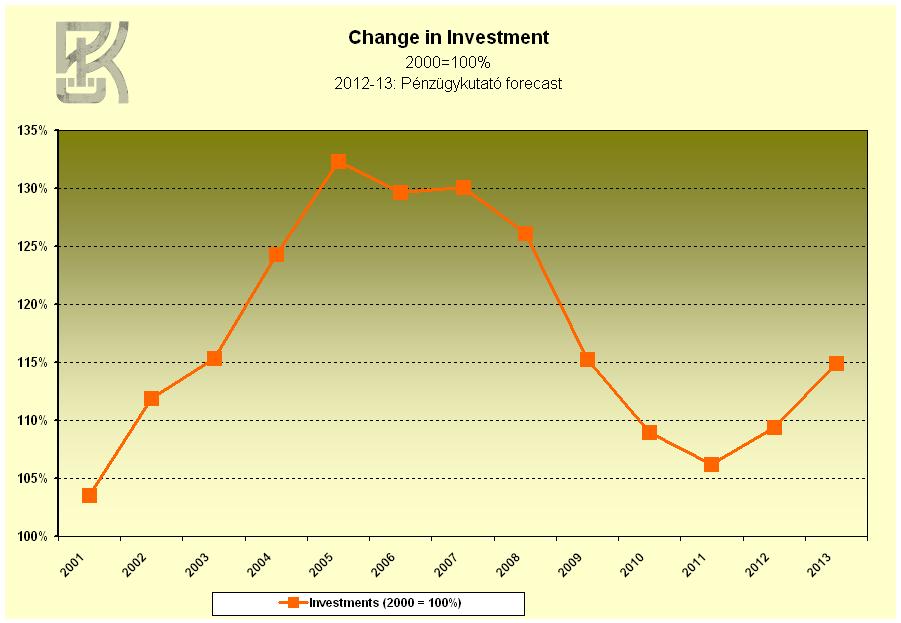

It was widely believed that the deterioration of the foreign positions will be balanced by 2-3% growth in investment.

The latest statistics show a 6.9% drop in the field.

There was a drop in the demand of households and in retail sales, too.

Investments may increase by 3% after this year?s drop but only because the end of the 7-year EU budget will make it necessary (though not more likely) to stimulate developments.

The corporate sector became net saver as opposed to the banks ? they save more than what they borrow.

It has been an international trend since Q3 2009 and the Hungarian government has been in line with that trend until the 2010 elections (Q2)

Neighbouring countries have seen a 4-8% investment growths since.

Greece and Spain show similar pattern in investments.

Hungary is thus in a severe position. This will make recovery even harder if not impossible.

Economic Outlook

Working Paper Series

-

11/26/2011 - 15:38

-

11/25/2011 - 16:00

-

11/18/2011 - 20:00

-

08/20/2011 - 15:31

-

07/18/2011 - 19:53