| Contact |  |

|

Economic Situation and Outlook of Hungary 2009-2010

Sponzored by

Budapest, 2009. September

Major characteristics of 2009

(World economy)

There are a growing number of indicators showing that the world economy might have hit rock bottom by the second quarter of 2009. The financial system has been on a slow way to recovery since May. Keynesian crisis management has reached its goal on the short run: Q2 GDP data indicate slowing pace of decline in the world economic centres. The Chinese economy has even showed strong growth by the middle of the year.

The annual rate of decline of the world GDP is expected at 1% - denying previously gloomy forecasts. The biggest output-decline is expected in Japan (-5.5%), both the Euro-area and the EU-27 could have a more moderate decrease at around -4%. US recession is expected less than 3% in the red, while the Chinese economy performs above expectations at a rate of +8%.

The effect of the output-decline to the employment is deferred. Unemployment is expected to decrease until the end of the year - long after production has hit rock bottom.

Global crisis coupled with deflationary tendencies - not least in the wake of fall in oil prices. Deflationary pressure has been strongest in Japan and the US, while the euro-area price levels remained nearly unchanged year-on-year. Annual average of oil prices are below last year's - despite pricing-in the currently positive economic news.

The volume of world trade will shrink by around 10% in 2009 compared to 2008 - despite encouraging signs in Q2 and the fact that strong protectionist turn has been avoided.

The crisis made direct capital flows decline.14% fall in 2008 has been followed by another 44% in Q1 2009. Decline is unlikely to turn out below 30% throughout the year despite improvement in the second half of the year.

The global financial crisis has created an immensely unfavourable environment for the Hungarian economy - in terms of investment, finance and the real economy. Only the external price trends have proved to be favourable. Easing financial and market tensions, however, indicate better conditions for the next year.

(Characteristics of the Hungarian economy)

The depth of the recession in 2009 recalls that of the transitional crisis. Then it was caused by internal changes in ownership and market structure - under more favourable international circumstances. This crisis, on the other hand, is the result of shrinkage in foreign credit and capital markets as well as our external export markets, further enhanced by restraint of domestic demand. Essential difference is that during the most difficult years of transition (between 1989-93) there was double-digit inflation, whereas now inflation has eased year-on-year - despite the increase in indirect taxation.

The dual effect of external and internal market losses resulted in a stronger-than-average recession within the EU. More difficult funding has also accelerated its pace. This is the reason Hungary suffers a delay in recovery - whilst in the more developed countries Q2 GDP data already indicate improvement.

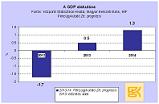

The recovery forecast for the second half of the year will more obviously be seen in Q4 - due to the base effect. After 7.2% decrease in the first half of the year we expect a 6% decline in GDP on annual average - with downward risk.

The decline extended to all sectors, most notably the export-oriented manufacturing. Least affected is the construction sector due to the commence of EU-projects and accelerated construction of new homes in the first half of the year. The biggest annual change occurred in agriculture, where GDP has grown by 50% in 2008 and there was an at least 15% decrease year-on-year on that basis. Non-commercial services suffered less decline than those related to the decrease in production (transport, trade, hospitality).

Significant changes in GDP-production on the demand side year-on-year:

- Household consumption reduced massively (by 6%) - in excess to decline on real wages (3-3.5%) The decline in real wages is far from dramatic - especially when compared to previous restriction years. Real incomes have depleted more than real wages due to the austerity measures of the Bajnai government. Household consumption comes under further pressure from unemployment near 10%, increased burden of debt-repayment on euro and Swiss frank- nominated loans (due to weaker Forint), and more cautious attitude of both the general public and the banks to debt and lending terms, respectively. Gross saving of households is expected to increase (as percentage of GDP) despite slowing increase in nominal income compared to 2008. This is due to reserve-building during crisis. Since the nominal borrowing of households will be lower than in 2008, the net savings rate (percentage of GDP) will increase to a level (4.2%) never before seen in Hungary.

- Decline in household consumption in Hungary exceeds that of the euro-area, the EU-27 averages and also that of the Visegrád countries. This is due to Hungary's higher exposure to the crisis and the difference in crisis management.

- Investment will fall by 4.5% (it was -2.6% in 2008). This is more moderate than the EU-average due to relatively quick attachment to EU funds. Foreign direct investment inflows will halve in 2009 - together with loans from owners - due to the negative investment climate.

- Stocks and inventories for sale and usage have depleted due to the shrinkage of markets and the difficulty of funding. Gross accumulation has declined by 39% in the first half of the year mainly due to the above. It is expected to be steeper than the decline in investments annually.

- The export-import in goods and services will shrink by more than 10%. Import cuts will be higher than the decrease in export due to the more significant shrinkage of the domestic market.

- Employment declines by 2.5%, the economy's productivity and the real wages by around 3% each.

The budget deficit will deteriorate compared to 2008. Deficit target was set at 2.9% of GDP in the 2009 budget (as opposed to 3.3% in 2008). The Gyurcsány-cabinet supposed it could be decreased to 2.6%. The IMF, however, has granted an easier target due to the larger-than-expected GDP-decline. The 3.9% deficit target still seems hardly achievable - due to the deficit in social security.

Import declines unusually heavily due to the decrease in both the import-intensive export and household spending and accumulation. Thus it improves the external balance during relatively deep recession - both nominally and as percentage of GDP. Current account deficit decreases from EUR 7.6 billion in 2008 to 2.6 billion in 2009 (7.2% and 2.7% of GDP, respectively).

Increasing surplus of capital account is due to EU funds, it decreases the country's external financing needs to EUR 0.9 billion (as opposed to 6.7 billion in 2008). Improved investor perception (of the country and the region) may have a favourable impact on non-debt financing in the second half of 2009.

We assume that funding can swing into positive territory again on annual average, to the extent of EUR 1.5 billion, which exceeds external financing needs by 60% thus reducing external debt.

The interest-reducing central bank policy characteristic for January must have halt during March due to extremely nervous investor moods - CDS premiums have reached their autumn peak again at 600 basis points and the euro exchange rate climbed to a critical level near 320 Forints. From May on, however, investor mood have improved gradually mainly due to steps taken by the Bajnai-government. CDS premiums started to decline, returns have decreased on both the government bond and the secondary markets on all maturities. The Central Bank has started cutting interest again in July based on favourable inflation outlook and strengthening confidence. Interest rate can decrease to 7% by the end of the year, the euro exchange rate can stabilize at around 275 Forints - provided that the Parliament adopts the 2010 budget.

2010 economic prognosis

Our 2010 economic forecast was based on the following assumptions:

(World economic conditions)

The world economy recovers from the crisis in 2010 according to our expectations. Stabilizing financial markets, stock market and credit flow revival will have a positive impact on the real economy. Strong fiscal and monetary stimuli will remain determining. The greatest upturn is expected in the US, where economy can grow by 2.1% in 2010 after 2.6% decline in 2009. The EU-27, the euro zone (1%) and Japan (1.5%) a more modest revival can be expected. China would only modestly accelerate its pace of growth, 8.5% as opposed to 8% in 2009. The world economy could return to its 2008 growth level at around 3%.

World trade would post a year-on-year growth again, but relatively depressed at around 3.5% in line with the GDP-growth. Direct investments would rise by 15%.

Deflationary risk ends in 2010 - with the exception of Japan. Inflation would rise again based on oil prices and additional demand pumped into the economies - it would not exceed 2% in the developed world. Oil prices would rise mostly on the basis of increasing Asian demand, we expect an annual average at around USD 90 per barrel.

While short-term trends improve, the medium-term solution of the global crisis remains questionable. The end of macroeconomic stimulus measures represents a risk, not knowing how and whether the organic growth based on the market could be restored - what strategies developed economies would chose to terminate the budgetary spending spree.

(Hungarian specifics)

The aim of economic policy is restoring and strengthening international confidence - achieving the performance targets and creating a foundation for future growth. Priorities are increasing employment, efficient utilisation of EU resources and supporting domestic businesses. We do not expect the new cabinet after the parliamentary election to substantially amend economic policies of the Bajnai-cabinet. Fiscal consolidation is expected to continue amidst harsh blaming on the predecessors, and a few symbolic decisions.

Monetary policy would ignore the single inflation hike, which is due in the first half of 2010 following the increase in indirect taxation. Further easing of interest rates would not have a major negative impact on investor confidence and the Forint exchange rates given the simultaneous tendency of rate increase throughout the world.

Fiscal policy seeks to meet the deficit targets imposed by the IMF and Brussels - which effort would be supported by the implicit reserves thanks to conservative targeting. The new cabinet could possibly even make a few symbolic decisions without threatening the deficit target.

It is possible that the new government would ease income restrictions - by compensational pay-rises in the public sector for instance. Expanding the range of income tax brackets and reducing the tax rates allows higher wage increase in net terms than in gross wages - despite the elimination of some tax breaks.

Unemployment rate could stop increasing on annual average if resources of the "Way to Work" (Út a munkába) Program is extended, the tax burden on wages decreased and further support to employment is provided.

EU funded investments would contribute to domestic demand to a larger degree than in 2009. But not even the expected 20% rise in foreign direct investment can offset losses in 2009 thus the level of investment would not reach that of 2008. We expect the Hungarian economy to increase its relative attraction to capital inflows.

Better income situation might improve the household savings level. Banks' lending-willingness will remain moderate, while households are expected to remain cautious in borrowing - net savings rate is expected to increase as percentage of GDP.

Improving economic outlook would increase demand for credit from businesses thus increasing their indebtedness to the banking system more than their savings rate is expected to improve. Borrowing surplus is expected to multiply compared to its 2009 level - which is part of returning to normal business and funding.

Summary

Restraint of domestic demand will still have an impact in 2010 as well as the improving international and external funding situation. The expected 0.5% GDP growth will be realised in a situation favourable in terms of growth and balance, if attributed to export and investments. The current account deficit will increase slightly, but the expected increase of EU transfers would raise the capital account balance to an estimated 2 billion therefore reducing the external financing requirement significantly (to EUR 700 million or 0.7% of GDP). Non-debt financing continues to grow as both direct and portfolio-investments can increase in a stabilizing economy.

The following growth pattern shows:

- Household demand will shrink further although slower than in 2009 - by 1-2%, due to the increased net savings of the population. This is a reaction to uncertainty during a crisis.

- Investments will increase by 1.5% - partly in line with export demand and because of higher EU transfers. Foreign direct investment will rise. Private property construction, however, will stagnate.

- Export of good and services will increase by 3% again, somewhat slower than the import.

- Structure of growth varies in each sector. Agriculture could revive by 5%, added value production of construction sector could expand by 4%. Industry, however, could lag behind due to only slow expansion on its domestic market. Service sector is expected to stagnate.

- External balance could worsen: trade balance surplus reduces to around EUR 3 billion, the balance of payments deficit increases by EUR 300 million.

- The budget deficit (ESA 95) will decline to 3.8% as proportion of GDP

- CPI decreases to 4% as annual average with around 3% by the end of 2010. Industrial price index is expected to grow in domestic sales due to energy price pressure and increasing demand in construction.

- Central Bank rate could drop to 5.75% by the end of 2010 - spread between credit and deposit rates can start tightening based on reducing lending risk for banks.

- HUF-EUR exchange rate is forecast at 274, HUF-USD at 183 by the end of 2010.

- Average gross wages will drop by 2% in the public sector, increase by 4% in the private. Real wages will increase by 2.1% compared to 2009.

- Productivity increases by around 1% amid 0.4% decrease in the employment base. Latter is within the statistical error range thus means stagnation. Unemployment will not grow as annual average.

- Domestic industrial sales stagnate, export grows moderately - the overall gross output of the sector grows by 1%.

- Gross output of construction grows by 3%.

- 5-7% growth can be expected in agriculture as a whole. Arable farming could grow by 5-10% in 2010 amid average weather conditions. Animal husbandry output would stagnate due to the slow process of reorganising the sector. Horticultural output is not expected to grow, but 10% growth in fruit production is possible.

- Retail sector could decrease by 1.3% (by EU standards, fuel prices included), much less than the 2009 decline.

Summary

(previous year= 100%)

(previous year= 100%)

| 2008 | 2009* | 2010* | |

| GDP growth | 100.6** | 94.0 | 100.5 |

| Investment | 97.4** | 95.5 | 101.5 |

| Household demand | 100.1** | 94.0 | 98.7 |

| Real income | 100.7 | 96.8 | 102.1 |

| Net savings growth of household - billion HUF | 223 | 1100 | 1200 |

| Industrial output | 100.0 | 85.0 | 101.0 |

| Construction output | 95.0 | 99.0 | 103.0 |

| Retail | 98.4 | 96.3 | 98.7 |

| Agriculture | 127.7 | 91.0 | 106.0 |

| Export (current price in EUR) | 105.6 | 81.0 | 103.0 |

| Import (current price in EUR) | 105.6 | 76.2 | 103.5 |

| Trade balance - billion EUR | -0.2 | 3.3 | 3.1 |

| Current account balance - billion EUR | -7.6** | -2.5 | -2.8 |

| Foreign direct investment with owners' loans - billion EUR | 3.1 | 1.5 | 1.8 |

| Budget deficit (ESA 95) as % of GDP | 3.3 | 4.0 | 3.8 |

| CPI annual average | 106.1 | 104.4 | 104.0 |

| Central Bank benchmark rate (end of year) | 10.0 | 7.0 | 5.75 |

| Yield on 3-month Treasury note (end of year) | 9.0 | 7.1 | 5.8 |

| HUF/EUR (end of year) | 264.8 | 275 | 274 |

| HUF/USD (end of year) | 187.9 | 190 | 183 |

| Unemployment (annual average) | 7.8 | 9.9 | 9.9 |

| Rate of employment | 98.8 | 97.5 | 99.6 |

* Financial Research forecast

** preliminary data

Source: Central Statistics Office (KSH), Central Bank of Hungary (MNB)

** preliminary data

Source: Central Statistics Office (KSH), Central Bank of Hungary (MNB)

Participants on the forecast:

Antalóczy Katalin, Juhász Pál, Halász György Imre, Mohácsi Kálmán, Petschnig Mária Zita, Várhegyi Éva, Voszka Éva.

Editor: Petschnig Mária Zita

Antalóczy Katalin, Juhász Pál, Halász György Imre, Mohácsi Kálmán, Petschnig Mária Zita, Várhegyi Éva, Voszka Éva.

Editor: Petschnig Mária Zita

Economic Outlook

Working Paper Series

-

11/26/2011 - 15:38

-

11/25/2011 - 16:00

-

11/18/2011 - 20:00

-

08/20/2011 - 15:31

-

07/18/2011 - 19:53